Sometimes a bit of anecdotal peer review is good for the soul

On Balance

On Balance

Sometimes a bit of anecdotal peer review is good for the soul

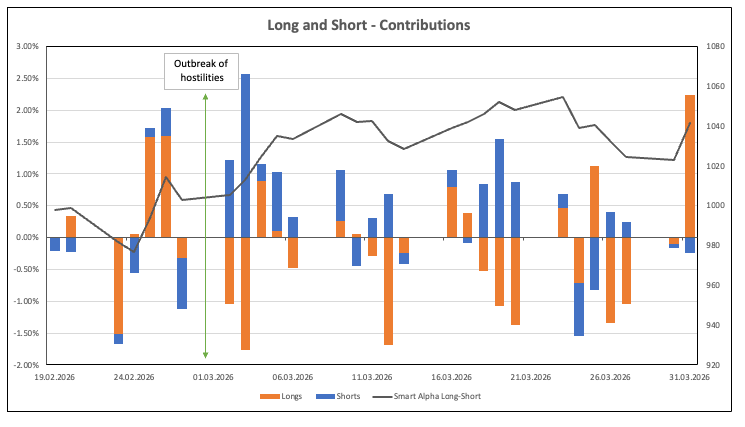

As markets nervously embrace the new conditions in the Middle East, we take the opportunity to review how our Smart Alpha strategies have fared in March 2026.

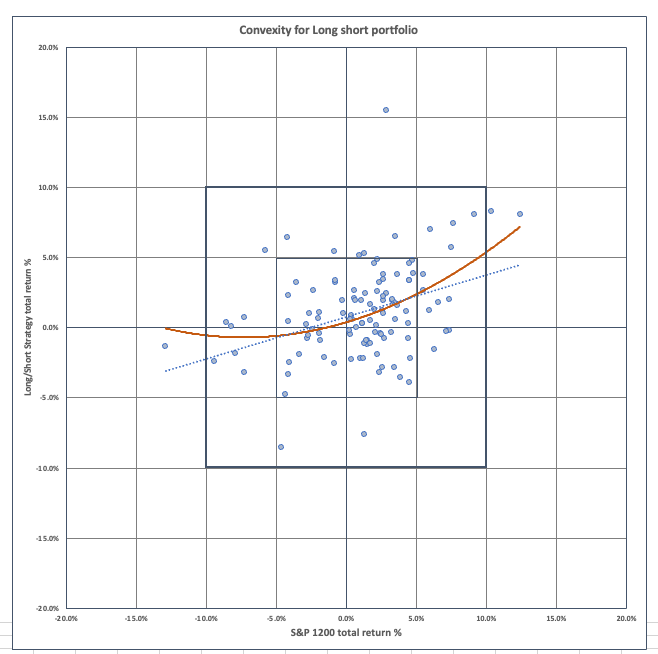

As equity investor concerns increase over lower beta return expectations from the market portfolio, increased levels of correlations between fixed income and equities and ever higher levels of benchmark concentration, the focus shifts to portfolio construction. By extending our existing Smart Alpha framework we have developed a set of positively convex, all equity portfolios that simultaneously magnify upside returns and hedge downside risks – providing a best-of-all worlds solution to equity risk and return.

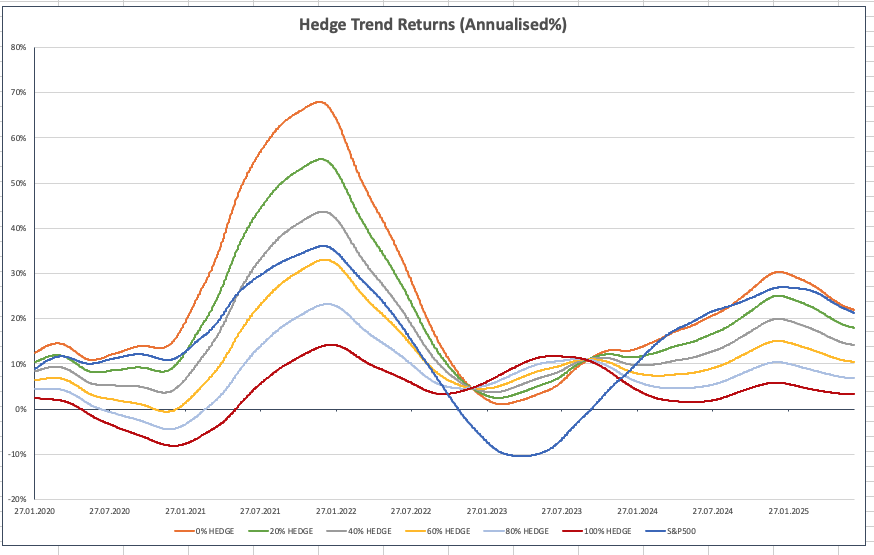

After last week’s discussion of Unknown Knowns, we update our findings and revisit the idea of how dynamically risk managing the portfolio’s exposure to underlying market risk can provide a more stable, compounding approach to investment returns.

Investment decisions are not just about Risk and Return – they are aboutindentifying the risks you DO NOT NEED TO TAKE. A focus upon the least appreciated of the Rumsfeld identities _Unknown Knowns – helps to shape our perception of the investment biases we do not need to follow if we want to maximise wealth.

After our latest portfolio rebalances we take a look at the “Weather” ahead

Portfolio construction needs to be about both a managed process of risk and return – not about multiple risks and multiple returns

There should be a better conversation about how to manage both risk and reward in equity markets.

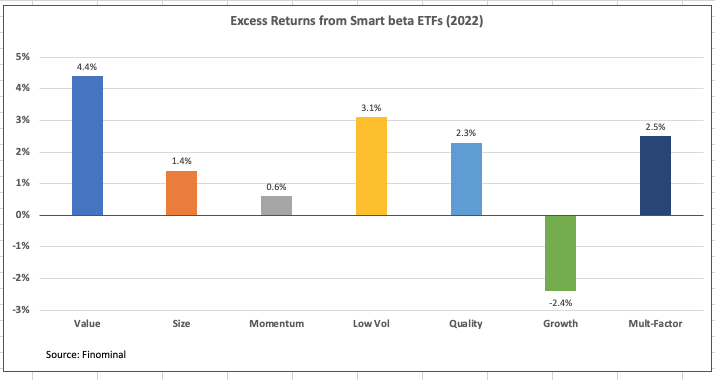

One of the most significant investment developments of recent years has been the emergence of factor-based investing as a mainstay of investment management.

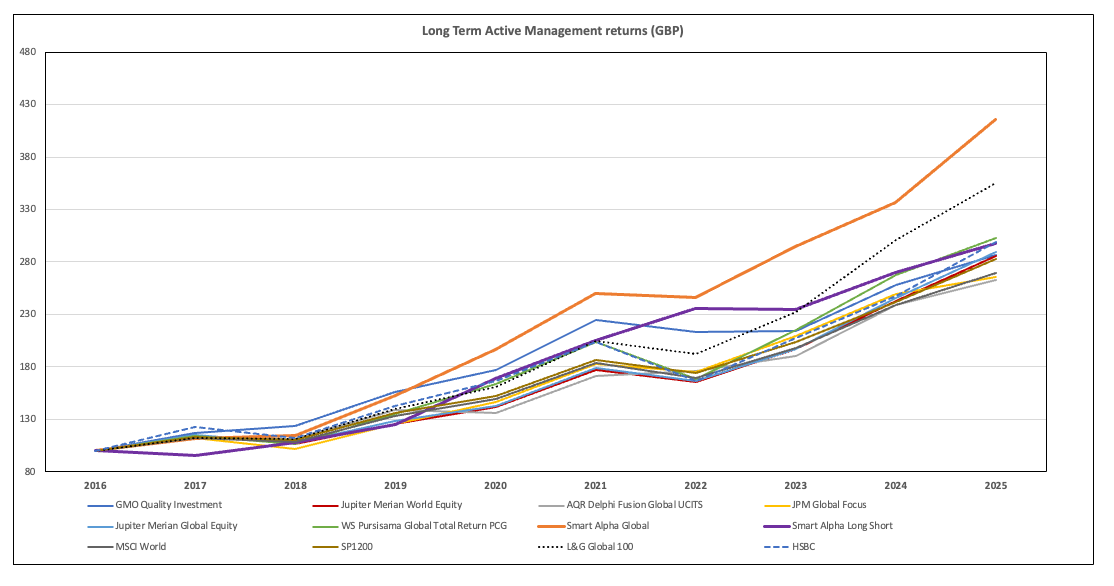

As we start a new Smart Alpha “Sprint period” for out S&P500 based Strategy, it is worth reviewing how we have performed so far this year.